Project Zero is not intended to be available for use, purchase, or access by U.S. persons, including U.S. citizens, residents, or persons in the United States of America, or companies incorporated, located, or resident in the United States of America, or who have a registered agent in the United States of America.

Blog · Core ideas

Blog #4: The Mechanics of Energy Markets

Part 4 of 5·Published on 5 Dec 2024

In our last post, we discussed how the grid itself operates – the physical infrastructure that delivers electricity from generators to end users.

We now consider a different question: how do we price the electricity that travels on this infrastructure?

Liberalisation of the Electricity Sector

As addressed in a previous post, fossil fuel power plants benefit from economies of scale, so it made sense for there to be a small number of coal- and oil-fired plants serving an entire country, facilitated by a national grid. For much of the twentieth century, the same firm that owned those plants also owned the grid, and sold electricity to consumers – a verticalised monopoly, typically under government ownership.

In the 1980s Chile was the first country to liberalise its electricity sector, breaking up its monopoly: electricity-generating plants were no longer owned by the same firm, but by multiple firms that competed for customers. A decade later, many European governments privatised the retail electricity side – the grid (both transmission and distribution networks) remained under monopoly ownership, but now consumers had a choice of suppliers and pricing models. Most countries have moved towards a state of liberalisation on both generation and retail supply sides.

The result of liberalisation is that private participants can trade with one another and, crucially, compete on price. This necessitated an auction system and a method of price discovery, the standard approach being marginal pricing. This auction also determines which generators are active for a given period, in turn determining the fuel mix – how clean or dirty the power is – during that period.

Such pricing ultimately flows into the rates you pay for your electricity as a customer, which is (generally) carefully bought by a retail supplier on your behalf. We examine these pricing mechanics below.

Merit Order and Wholesale Pricing

Marginal pricing is used for price discovery in most modern electricity wholesale markets. This means electricity prices for each period are set by the variable cost of the marginal plant, i.e. when ranked by price, the price of the most expensive plant required to meet demand.

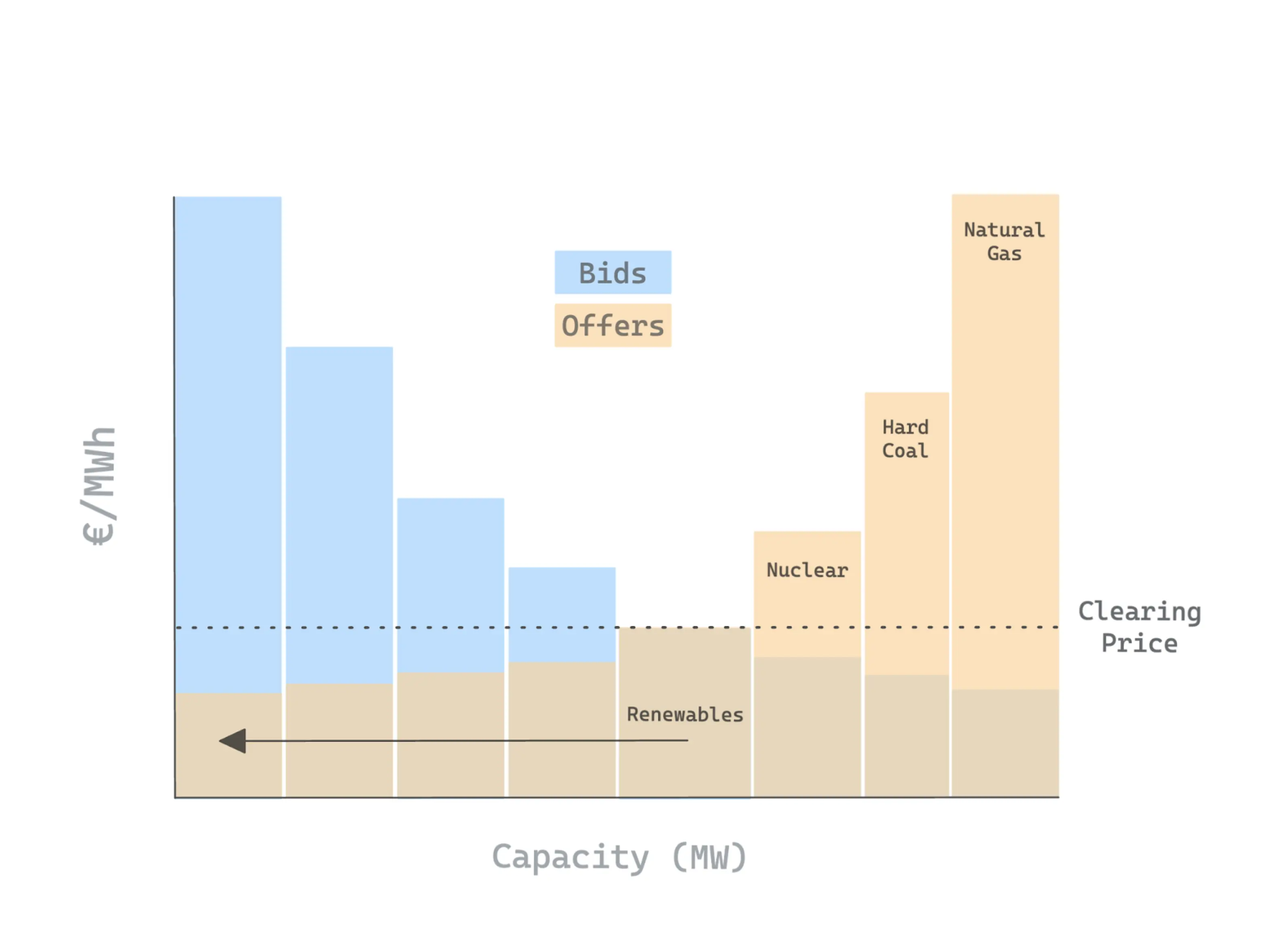

The model works as follows: for a specific time period (generally a half hour or fifteen minute period) generators offer a volume of electricity at a given price, and retail companies bid for volumes at a price they’re willing to pay (more on the demand side in a future post). Offers from market participants are ranked by price in ascending order. This is known as the merit order.

Once ranked, the price is set by the generator offer which intersects the supply-demand equilibrium. This is themarginal or clearing price for the period, and every volume cleared will settle at this marginal price, regardless of the original bid or offer.

The graph below illustrates this. Each energy generator has offered a given volume of electricity into the auction at a given price, and these offers are price-ranked. At the same time, retail electricity companies and offtakers have submitted bids for their demand requirements, resulting in a demand curve. Where the demand curve meets the merit order stack is the price the market will clear at that period, i.e. the price everyone will pay for that half hour or 15 minutes. In essence, the last MW of power that turns on is the one that sets the price for everyone in the market.

Currently, renewable production is very cost efficient, and typically makes the cheapest offers when available. The key reason for this, other than subsidies and carbon pricing, is because renewable generation has zero marginal costs. A solar farm’s fuel – sunlight – is free, unlike natural gas. Turning on, or up, is free for solar plants, not for gas ones.

Accordingly, when renewable production is available to fully meet demand, the marginal price is often set by the price of wind or solar power. However, during overnight periods of high atmospheric pressure, resulting in limited wind, the marginal price is set by gas (or occasionally coal in regions where it has not been phased out of supply).

As renewables make up more of the generation stack, fossil fuels are gradually being pushed out. The less often fossil fuels have their orders filled, the higher the price they need to charge to recover their fixed costs. The net effect of this is that, as renewable deployment progresses, we see a widening spread between the price of periods when renewables set the price, and periods when fossil fuels do. This presents an opportunity.

Hedging and Retail Pricing

In addition to the process we just outlined, prices in electricity markets already experience significant volatility. This is due to a variety of fundamental short term factors, including changes in demand, commodity prices, supply chains, macroeconomic influences, and weather. These impact both demand and renewable availability.

The effects of volatility were acutely seen in Texas in 2021, when Storm Uri took generation capacity offline resulting in extreme intraday volatility. Prices reached $9,000/MWh and stayed there for almost four days, orders of magnitude above the 10 year average of $40-$60/MWh. In addition to the deployment of renewables filling up more of the generation stack, volatility is being exacerbated more widely by burgeoning demand, proportional reduction in firm capacity, and an increasing frequency of natural disasters.

The resulting volatility poses existential risks to the operations of retail suppliers, who are obliged to deliver power to their customers, often at a capped rate. To protect themselves, suppliers hedge their obligations by buying electricity in advance, generally through forward contracts. Forward markets allow participants to lock in electricity prices for future delivery periods, providing a safeguard against the unpredictability of day-ahead and imbalance prices.

Hedges are almost always priced at the marginal gas price. Because long range weather forecasts are not reliable, the market prices electricity in the forward market in the UK at close to the marginal gas price, even if there is an expectation of some renewable generation in the delivery period. The trick with hedging with a combination of forwards and clean energy assets is modelling customer demand and the production of clean energy assets.

Firms do get this wrong, sometimes with disastrous results – a most spectacular example is that of the startup Bulb, which became national news in 2021 after it required a £6 billion bailout from the UK government.

Hedging enables a supplier to fix the price their customers will pay through a billing period. This price is generally a function of the supplier’s aggregate hedged position in that location. As we approach delivery, that hedge may be above or below the price on the short term day-ahead market. In other words, it can be in or out of the money. Historically customer demand was inflexible, and so a supplier would be forced to deliver power even when they could see much greater profits in selling the hedge into the day ahead market. However this is beginning to change.

Some suppliers have attempted to give customers exposure to day-ahead prices via indexed or spot tariffs, where customers essentially pay the wholesale rate plus a margin. This however, can give the customer no protection from price volatility – they are unhedged, naked, and susceptible to great swings in their rates. After Storm Uri, some suppliers passed on wholesale rates to Texas customers that resulted in residents receiving $16,000 bills for a month’s electricity.

This kind of pricing requires a sophisticated customer to actively change their usage based on price, otherwise they’ll often be worse off. The typical version of these tariffs doesn’t provide adequate protection for most retail users.

But this increasing volatility does present an opportunity. Instead of riding the wholesale price with full exposure, what if we started from a hedged position, then traded out of that position when the hedges are in the money and profitable to resell, or bought more at cheaper wholesale rates when the hedges are out of the money? This can be possible through coordination between suppliers and their customers to shift loads on the demand side. The result being a lower cost of electricity for the supplier, which can be passed down to the customer. Project Zero is putting this into production.

This supplier-user coordination is known as demand response, and is a core component of Project Zero. While making the grid greener and more flexible, it also delivers economic benefits under current electricity market dynamics. It aligns incentives perfectly, which we will explore more in a future post.